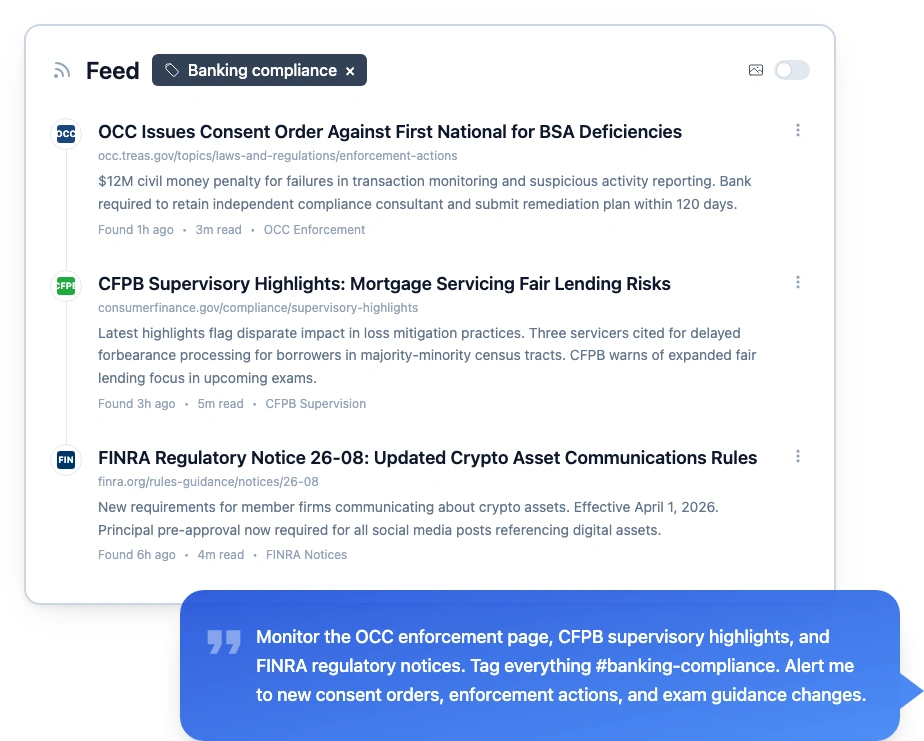

Banks answer to 6+ federal regulators and 50 state agencies. Here's how finserv compliance teams track regulatory changes without missing updates that trigger enforcement.

Regulatory Change Tracking for Financial Services

In 2024, the OCC fined banks $1.5 billion. The CFPB returned $3.2 billion to consumers. The SEC collected $8.2 billion in penalties. And those are just three of the agencies that oversee financial services.

The core problem isn't that compliance teams don't care. It's that they can't watch everything. A mid-size bank might answer to the OCC, CFPB, FINRA, SEC, FinCEN, the Federal Reserve, FDIC, and 15 state regulators. Each publishes rules, guidance, enforcement actions, and exam priorities on its own website, on its own schedule. Miss one update on one page, and you're exposed.

This guide covers which agencies matter, what to monitor on each, and how to build a regulatory compliance monitoring system that catches changes across all of them.

Why Financial Services Is Different

Every industry faces regulation. Financial services faces regulation from everyone, all at once.

A national bank chartered by the OCC is also supervised by the CFPB for consumer products, the SEC for securities activities, FINRA for broker-dealer operations, FinCEN for anti-money laundering, and the Federal Reserve for holding company oversight. State-chartered banks add their state banking department to the list.

These agencies don't coordinate their publication schedules. The OCC might update examination guidance on a Tuesday. The CFPB could issue a supervisory highlight the same afternoon. FinCEN might publish a new advisory on Thursday. Each change could affect the same compliance program, from different angles, with different deadlines. Government regulatory monitoring across all of these simultaneously is the baseline requirement.

The result: financial services compliance teams face more overlapping regulatory exposure than any other industry. A single missed update can trigger enforcement from multiple agencies. And unlike pharma (primarily FDA) or healthcare (primarily CMS), there's no single primary regulator to watch. You watch them all or you accept the risk.

Monitor regulatory pages automatically

Changeflow watches agency websites and tells you what changed and why it matters.

Free plan available. No credit card required.

The Agencies and What to Track

Not every page on every regulator's website matters. Here's what compliance teams should actually monitor on each.

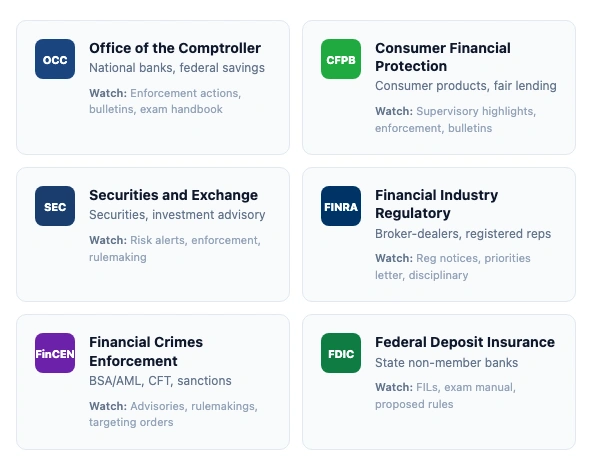

OCC: National Bank Supervision

The OCC supervises national banks, federal savings associations, and federal branches of foreign banks. It issues the most enforcement actions of any banking regulator.

What to monitor:

- Enforcement actions page (consent orders, cease-and-desist, civil money penalties)

- Bulletins and news releases

- Comptroller's Handbook updates (exam procedures)

- OCC Interpretive Letters (legal opinions on permissible activities)

Why it matters: OCC enforcement actions against one bank signal where examiners will focus next at others. When the OCC issues a consent order for BSA/AML deficiencies, every other national bank should expect heightened scrutiny in their next exam.

CFPB: Consumer Protection

The CFPB oversees consumer financial products: mortgages, credit cards, auto loans, student lending, and deposit accounts.

What to monitor:

- Supervisory highlights (anonymized exam findings, published quarterly)

- Enforcement actions

- Compliance bulletins and policy guidance

- Advisory opinions

- Proposed and final rules

Why it matters: CFPB supervisory highlights are the closest thing to a public exam playbook. When the CFPB flags "unfair practices in auto lending servicing" in its highlights, that's a preview of where the next enforcement sweep will focus. Teams doing regulatory change management should treat each supervisory highlight as an early warning.

SEC: Securities Regulation

The SEC regulates securities activities including broker-dealer operations, investment advisory, and public company disclosure. We've covered SEC filing monitoring in depth. For regulatory tracking specifically:

What to monitor:

- Division of Enforcement litigation releases

- Staff guidance and no-action letters

- Proposed and final rulemaking

- Risk alerts from the Division of Examinations

- Commissioner speeches (signal upcoming enforcement priorities)

Why it matters: SEC risk alerts from the Division of Examinations are the single best predictor of what examiners will focus on. When the SEC publishes a risk alert about marketing rule compliance, every registered investment adviser should review their marketing materials before the next exam.

FINRA: Broker-Dealer Oversight

FINRA is the self-regulatory organization for broker-dealers. It publishes regulatory notices, enforcement actions, and exam priorities that affect every registered broker-dealer and their associated persons.

What to monitor:

- Regulatory notices (new rules, rule amendments, guidance)

- Disciplinary actions

- Annual regulatory and examination priorities letter

- Trade reporting notices

Why it matters: FINRA's annual priorities letter is effectively a roadmap for the year's exams. The priorities letter published in January tells you exactly which areas FINRA will scrutinize. Firms that read it and self-assess before the exam consistently fare better.

FinCEN: Anti-Money Laundering

FinCEN administers the Bank Secrecy Act and enforces AML/CFT requirements. BSA/AML is the single most common source of enforcement actions across all banking regulators.

What to monitor:

- Advisories (alerts about specific money laundering typologies)

- Rulemakings (beneficial ownership, customer due diligence)

- Administrative rulings

- Geographic targeting orders

Why it matters: FinCEN advisories describe specific threat patterns. When FinCEN publishes an advisory on human trafficking-related financial activity, banks need to update their transaction monitoring rules and train front-line staff. Missing an advisory doesn't just create compliance risk. It creates real harm.

Federal Reserve and FDIC

The Federal Reserve supervises bank holding companies and state member banks. The FDIC supervises state-chartered non-member banks.

What to monitor:

- Fed: Supervision and Regulation (SR) letters, Community Banking Bulletin

- FDIC: Financial Institution Letters (FILs), consumer compliance exam manual updates

- Both: Proposed rules, interagency statements, stress testing guidance

Why it matters: SR letters and FILs are how these agencies communicate expectations to the banks they supervise. An SR letter on model risk management applies to every bank holding company. A FIL on third-party risk management affects every FDIC-supervised institution.

The Hidden Volume Problem

Formal rulemaking in the Federal Register is what most people think of when they hear "regulatory changes." But in financial services, formal rules represent maybe 20% of what compliance teams need to track.

The other 80% happens on agency websites:

- Enforcement actions that signal shifting priorities

- Supervisory guidance that changes how existing rules are interpreted

- Exam manual updates that tell examiners what to look for

- No-action letters that clarify permissible activities

- Speeches and testimony that preview upcoming rulemaking

- Interagency statements that coordinate expectations across regulators

This is the "horizon scanning" problem. Formal rules have predictable timelines: proposed rule, comment period, final rule. But a CFPB supervisory highlight or an OCC bulletin can change compliance expectations overnight, with no comment period and no advance notice.

Teams that only monitor the Federal Register and their GRC platform's regulatory feed are flying partially blind. The most actionable intelligence lives on agency web pages. See our regulatory compliance examples for specific cases where agency website changes triggered compliance obligations before any formal rulemaking.

Building a Multi-Agency Monitoring System

Here's a practical setup for financial services compliance teams. Start small. You can expand later.

Step 1: Map Your Regulatory Universe

List every agency that has jurisdiction over your institution. A typical community bank might have:

- OCC or state banking department (primary regulator)

- FDIC (deposit insurance)

- CFPB (consumer products, if >$10B in assets)

- FinCEN (BSA/AML)

- State AG consumer protection division

- Potentially SEC and FINRA (if securities activities)

A large bank holding company might add the Federal Reserve, multiple state regulators, and international supervisors. The list matters because it defines your monitoring scope.

Step 2: Identify the Pages That Matter

For each agency, identify 3-5 specific web pages to track website changes on. Not the homepage. The specific pages where enforcement actions, guidance, and exam updates appear.

For example, for the OCC:

- Enforcement actions listing page

- OCC Bulletins page

- News releases page

- Comptroller's Handbook page (exam manuals)

That's 4 pages. Do the same for each agency. A bank supervised by 5 agencies ends up monitoring 15-25 specific pages. That's manageable.

Step 3: Set Up Monitoring with AI Filtering

Use a change detection tool to watch each page. With Changeflow, the process for each page is:

- Add the URL as a source

- Write a brief: "Alert me to new enforcement actions, guidance updates, and exam manual changes. Ignore navigation updates and formatting changes."

- Route website alerts to the compliance team member responsible for that regulator

- Tag sources by agency (OCC, CFPB, SEC) for filtering

The AI reads each page change and decides whether it matches your brief. A menu reorganization gets filtered out. A new consent order gets flagged and summarized.

Step 4: Build Response Workflows

Detection without a response process creates a backlog. Define what happens when a regulatory change is detected:

| Change Type | Response Time | Who Reviews | Action Required |

|---|---|---|---|

| Enforcement action (own institution) | Immediate | General counsel, CCO | Board notification, remediation plan |

| Enforcement action (peer institution) | Same day | Compliance analyst | Gap assessment against findings |

| New rule or guidance | 48 hours | Subject matter expert | Impact assessment, policy review |

| Exam manual update | 1 week | Compliance analyst | Control mapping update |

| Supervisory highlights | 1 week | CCO, compliance team | Self-assessment against findings |

Step 5: Review and Expand

After 30 days, review what you caught and what you missed. Add state regulator pages. Add industry association updates (ABA, ICBA). Consider adding banking intelligence sources for competitor and market tracking.

Common Mistakes

Relying on a Single Regulatory Feed

Most compliance monitoring software and GRC platforms offer a regulatory content feed. These feeds are curated from formal sources: Federal Register, state legislative databases, and regulatory filings. They typically miss:

- Agency website guidance updates

- Enforcement action details (beyond the headline)

- Exam manual revisions

- Staff no-action letters and interpretive guidance

A single feed is a starting point, not a solution. Layer it with direct source monitoring for your primary regulators.

Monitoring Only Your Primary Regulator

Your primary regulator (OCC, FDIC, or state banking department) gets the most attention. But the CFPB, FinCEN, and SEC can each independently bring enforcement actions against you. An OCC-supervised bank that ignores CFPB supervisory highlights is missing a critical signal.

No Process for Interagency Guidance

Interagency statements (published jointly by two or more regulators) can change compliance expectations for the entire industry overnight. The 2023 interagency statement on crypto-asset risks effectively ended banking services for crypto companies. If you're only monitoring each agency individually, you might catch the statement on one site and miss it on others, creating confusion about which version is authoritative.

Treating All Changes Equally

Not every regulatory update requires the same response. A FinCEN advisory about a new money laundering typology needs immediate attention from your BSA team. An OCC bulletin about reporting format changes can wait for the next compliance committee meeting. Triage is essential, and it's where AI filtering adds the most value.

What Financial Regulatory Tracking Costs

Free tier: Each agency offers some form of alert. FINRA regulatory notice emails, OCC news release RSS, FinCEN email alerts. These cover formal publications but miss website content changes and provide no filtering.

Mid-range ($99-200/month): Website monitoring tools like Changeflow that watch specific agency pages with AI filtering. Cover both formal publications and informal guidance updates. Good for the regulatory intelligence awareness layer.

Enterprise ($50,000-200,000+/year): FiscalNote, Thomson Reuters Regulatory Intelligence, and CUBE provide pre-indexed multi-agency coverage with obligation mapping, analyst commentary, and workflow tools. Strong on financial services-specific coverage.

Most mid-size banks start with the mid-range tier for direct source monitoring and add enterprise tools as compliance headcount and regulatory complexity grow. The two aren't mutually exclusive. Enterprise platforms give you curated intelligence. Direct source monitoring catches what the curated feeds miss.

Getting Started

If you're a financial services compliance team building regulatory tracking for the first time:

- List your regulators (typically 4-6 agencies)

- Identify 3-5 specific pages per agency (enforcement, guidance, exam updates)

- Set up change monitoring with AI filtering on each page

- Define response workflows by change type

- Review results monthly and add sources as gaps appear

You can be monitoring your top regulatory sources within an hour. Start with the highest-risk pages (SEC staff guidance, OCC bulletins, CFPB supervisory highlights, FINRA regulatory notices, FinCEN advisories) and add agencies as you go. The compliance teams that catch regulatory changes early don't have bigger budgets. They just built a system that watches the right pages and tells them when something actually matters.

That's the difference between learning about a new OCC consent order from your examiner and reading it the day it was published.

Frequently Asked Questions

What regulators do banks need to monitor?

At minimum: the OCC (national banks), FDIC (state-chartered insured banks), Federal Reserve (bank holding companies), CFPB (consumer protection), SEC (securities activities), FINRA (broker-dealer operations), and FinCEN (BSA/AML). State-chartered banks also answer to their state banking department. Most banks face oversight from 4-6 of these simultaneously, each publishing rules, guidance, and enforcement actions independently.

How often do financial regulations change?

More frequently than most teams realize. The Federal Register publishes 20-30 financial services-related notices per week. But the bigger volume comes from agency websites: enforcement actions, examination guidance, supervisory highlights, no-action letters, and FAQ updates. The OCC alone issued 180+ enforcement actions in 2024. Most compliance teams undercount because they only watch formal rulemaking.

What is the cost of missing a regulatory change in banking?

Penalties range from tens of thousands to billions. The OCC fined banks $1.5 billion in 2024. The CFPB returned $3.2 billion to consumers. The SEC collected $8.2 billion in penalties. Beyond fines, missed changes can trigger consent orders, business restrictions, and reputational damage. Regulators increasingly expect proactive compliance, not reactive correction after examination findings.

Can AI help with financial regulatory tracking?

Yes. AI helps at two levels. First, it monitors agency websites and filters routine updates from material changes. When the OCC changes a page, AI reads the content and decides whether it affects your compliance obligations. Second, it summarizes changes in plain language so compliance analysts don't need to read every source document. The human still decides what to do about it.

What's the difference between regulatory tracking and a GRC platform?

Regulatory tracking detects external changes: new rules, amended guidance, enforcement trends. A GRC platform manages internal compliance: policies, controls, audits, and remediation workflows. You need both. The tracking tool tells you something changed. The GRC platform helps you respond. Many banks use Changeflow or FiscalNote for tracking, and MetricStream or Archer for the GRC workflow.

Track financial regulatory changes automatically

Monitor SEC, OCC, CFPB, FINRA, and state regulator websites. AI filters noise and summarizes what matters for your compliance program.

Try Changeflow FreeNo credit card required

More from Learn

Wayback Machine for Legal Research: A Law Librarian's Guide

Half the URLs in old briefs are dead. Here is how law librarians use the Wayback Machine and stronger archives to verify citations, build timelines, and support litigation.

Law Librarian Current Awareness Audit Checklist (2026)

A 27-question audit covering coverage, cadence, relevance, distribution, resilience, and value. Built for law librarians and knowledge lawyers running current awareness at Am Law 200 firms.

Audit-Ready Web Archives: SEC 17a-4, FDA, and HIPAA Rules

Free archive tools fail under regulatory audit. Here is what SEC 17a-4, FDA 21 CFR Part 11, and HIPAA require from a web archive that holds up under examination.